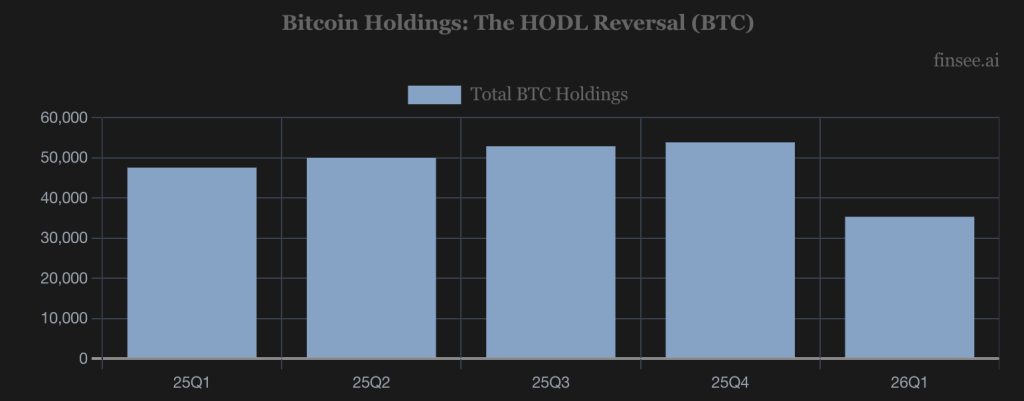

Marathon Digital Holdings, the largest Bitcoin Mining miner in America, has reportedly sold approximately $1.5 billion in Bitcoin, offloading roughly 20,880 BTC at an average price near $70,137 per coin, and announced it will not purchase additional mining hardware, pivoting instead toward AI infrastructure.

MARA stock was up 0.24% at the time of reporting, while BTC-USD was down 1.39%. Bearish signal for corporate Bitcoin treasury models.

The sale reduces MARA’s holdings from 38,689 BTC to approximately 35,303 BTC, ranking the company fourth among public Bitcoin holders.

Proceeds were used to repurchase convertible notes at a discount, cutting total debt from $3.3 billion to $2.3 billion, a 30% reduction, and generating a $71 million accounting gain. Q1 revenue fell 18% year-over-year to $174.6 million amid a $1.26 billion net loss.

How a $1.5B Bitcoin Mining Sale Works Mechanically, and Why the Timing Matters

MARA’s reported sale represents roughly 54% of its former Bitcoin stack by coin count, executed in tranches with 15,133 BTC ($1.1 billion) sold between March 4 and March 25, 2026.

At current market prices, the remaining 35,303 BTC is valued at approximately $2.84 billion. That is a meaningful reserve. It is not the treasury-first posture the company was signaling 12 months ago.

The mechanics of the debt repurchase matter here. By retiring convertible notes at a discount, MARA locked in a $71 million accounting gain while simultaneously removing the interest burden that made the Saylor-style treasury model increasingly fragile at post-halving mining margins.

CEO Fred Thiel did not abandon Bitcoin. He used it as liquidity to stabilize a balance sheet that $3.3 billion in convertible notes had stretched thin.

That distinction is worth naming. Selling Bitcoin to service debt is operationally rational under margin pressure. It is not the same as abandoning a thesis. Those are not the same thing, and conflating them leads to the wrong analytical conclusion.

Does a $1.5B Sale Signal a Break in MARA’s Bitcoin Conviction – or Operational Cash Management?

Two readings compete here. The bearish read: MARA raised a convertible note explicitly to emulate Michael Saylor’s Bitcoin treasury accumulation strategy, then reversed course and liquidated a substantial portion of its stack within two earnings cycles.

If the conviction were genuine, the company would have found alternative debt service mechanisms rather than selling BTC near cycle lows.

The pivot to AI is a rebranding exercise covering a treasury model that failed stress testing.

The operational read: MARA produced 2,247 BTC in Q1 while simultaneously boosting its energized hashrate 33% year-over-year to 72.2 EH/s. It is still mining aggressively.

The $1.5 billion in AI infrastructure spending – anchored by a ~$1.5 billion acquisition of Long Ridge Energy’s 505-MW natural gas plant in Hannibal, Ohio, expected to yield $144 million in annual EBITDA – is not a retreat from hard assets. It is a rotation from one capital-intensive physical infrastructure play to another, with better margin economics in the current rate environment.

Scott Melker, host of The Daily Wolf on Yahoo Finance, framed the industry trajectory bluntly: “Bitcoin miners are no longer Bitcoin miners, they are AI companies that will also mine Bitcoin.”

That is not an indictment of Bitcoin conviction. It describes where the capital returns are. Bitcoin Society recent pause on Bitcoin treasury acquisition reflects a similar dynamic, corporate conviction around BTC holdings is being stress-tested across multiple balance sheets simultaneously, not just MARA’s.

The provisional conclusion: MARA’s sale is primarily a debt management event with a strategic pivot embedded inside it. The treasury model stress is real. The conviction collapse narrative is overstated.

The post Bitcoin Mining: MARA’s Reported $1.5B Bitcoin Sale Puts Corporate Treasury Conviction in Focus appeared first on Cryptonews.