| Invesloan.com")

The S&P 500 (SP500) on Friday superior 0.77% for the week to shut at 4,594.63 factors, posting positive aspects in three out of 5 periods. Its accompanying SPDR S&P 500 Trust ETF (NYSEARCA:SPY) added 0.83% for the week.

During this week, Thursday marked the top of November, a month that turned out to be historic for markets. The benchmark S&P (SP500), together with the Nasdaq Composite (COMP.IND) and the Dow (DJI), notched their greatest month-to-month advance this yr and certainly one of their greatest Novembers on document.

That climb has been largely pushed by favorable financial information and feedback from Federal Reserve audio system that has led to a common consensus that the central financial institution is finished mountain climbing charges and may ship a comfortable touchdown – an occasion the place inflation comes down with out compromising employment or progress.

The same pattern contributed to this week’s positive aspects and has led to the S&P 500 (SP500) notching its highest closing degree of the yr. This leaves the market poised for a powerful end to the yr with Friday being the primary day of December. Investors will hope that November’s momentum can lengthen right into a “Santa Claus” rally.

The week began off with the retail sector in focus, after Cyber Monday adopted final week’s Black Friday in setting new data for spending. Two financial indicators grabbed a lot of the highlight on Wednesday and Thursday – first, the second estimate of U.S. Q3 GDP progress was revised increased. Then, Thursday’s private earnings and outlays report confirmed a M/M and Y/Y moderation within the Fed’s most popular inflation gauge – the non-public consumption expenditures value index. Both units of information significantly strengthened comfortable touchdown hopes.

Fed chair Jerome Powell garnered consideration on Friday with some feedback at a hearth chat at Spelman College. Powell in his opening remarks tried to tamp down the market’s enthusiasm when it comes to fee cute expectations, saying that it was nonetheless too “premature” to conclude that financial coverage was sufficiently restrictive. However, as soon as the hearth chat began, Powell’s replies to questions had been much more optimistic and all however confirmed to merchants that the central financial institution wouldn’t hike charges anymore.

In the lead-up to Powell, there was notable optimistic commentary from Fed Governor Christopher Waller on Tuesday and Chicago Fed President Austan Goolsbee earlier at the moment.

The continued favorable financial information additionally led to buyers snapping up bonds this week, driving Treasury yields decrease and serving to equities. The longer-end 10-year yield (US10Y) has slipped 26 foundation factors whereas the shorter-end extra rate-sensitive 2-year yield (US2Y) has slid 40 foundation factors. The demand for bonds additionally obtained a detailed examination within the type of Treasury word auctions this week – a $54B 2-year public sale on Monday tailed whereas a $55B 5-year public sale traded via. Tuesday’s $39B 7-year public sale tailed by a major margin.

See how Treasury yields have performed throughout the curve on the Seeking Alpha bond web page.

Turning to the weekly efficiency of the S&P 500 (SP500) sectors, 9 of the 11 ended within the inexperienced, led by an outsized soar of about 5% in Real Estate. Communication Services and Energy had been the highest losers. See under a breakdown of the efficiency of the sectors in addition to their accompanying SPDR Select Sector ETFs from November 24 near December 1 shut:

#1: Real Estate +4.99%, and the Real Estate Select Sector SPDR ETF (XLRE) +4.65%.

#2: Materials +2.57%, and the Materials Select Sector SPDR ETF (XLB) +2.75%.

#3: Industrials +2.14%, and the Industrial Select Sector SPDR ETF (XLI) +2.26%.

#4: Financials +2.09%, and the Financial Select Sector SPDR ETF (XLF) +2.23%.

#5: Consumer Discretionary +1.48%, and the Consumer Discretionary Select Sector SPDR ETF (XLY) +1.69%.

#6: Utilities +1.27%, and the Utilities Select Sector SPDR ETF (XLU) +1.34%.

#7: Consumer Staples +0.55%, and the Consumer Staples Select Sector SPDR ETF (XLP) +0.77%.

#8: Health Care +0.48%, and the Health Care Select Sector SPDR ETF (XLV) +0.53%.

#9: Information Technology +0.34%, and the Technology Select Sector SPDR ETF (XLK) +0.63%.

#10: Energy -0.11%, and the Energy Select Sector SPDR ETF (XLE) +0.11%.

#11: Communication Services -2.49%, and the Communication Services Select Sector SPDR Fund (XLC) -1.48%.

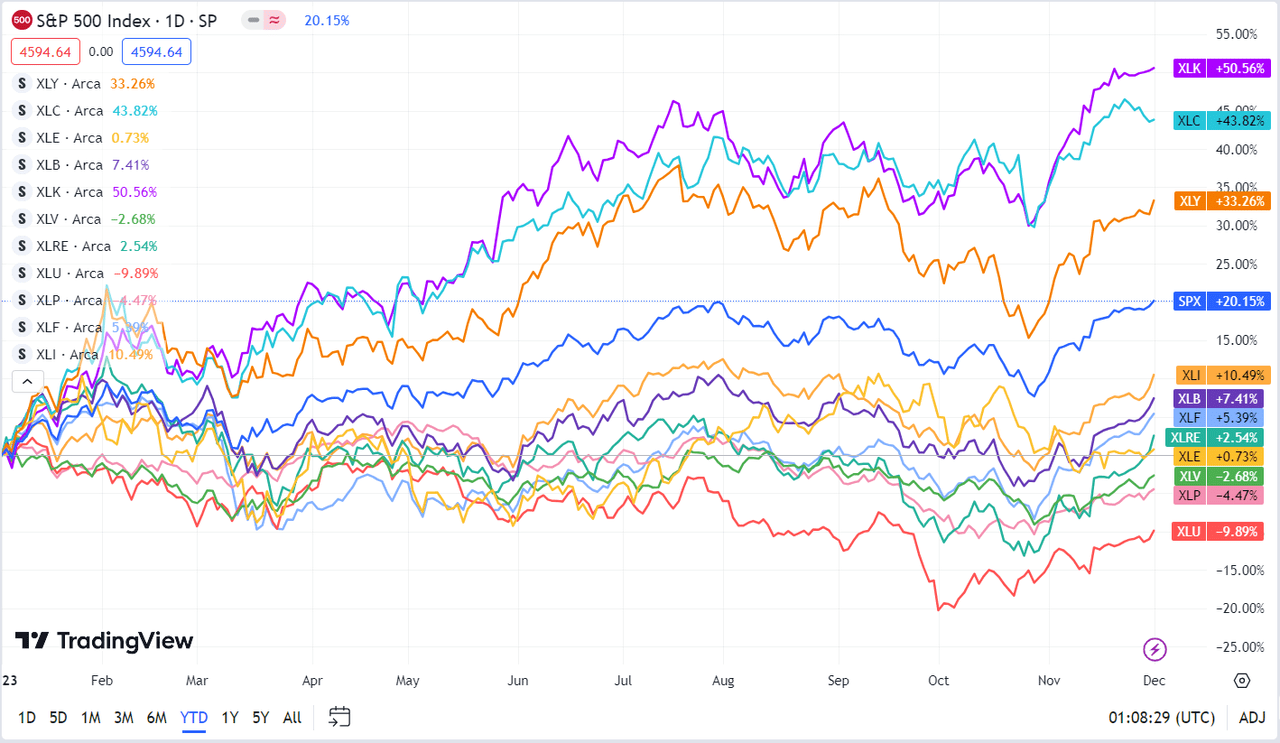

Below is a chart of the 11 sectors’ YTD efficiency and the way they fared in opposition to the S&P 500 (SP500). For buyers wanting into the way forward for what’s taking place, check out the Seeking Alpha Catalyst Watch to see subsequent week’s breakdown of actionable occasions that stand out.