A change in technique has helped remodel the GoodHaven Fund from a long-term underperformer into an outperformer because the finish of 2019. The fund follows a concentrated-value method and now has a four-star ranking (out of 5) in Morningstar’s Large Blend fund class.

Larry Pitkowsky, managing companion of GoodHaven Capital Management, based mostly in Millburn, N.J., defined how this was achieved in an interview with MarketWatch.

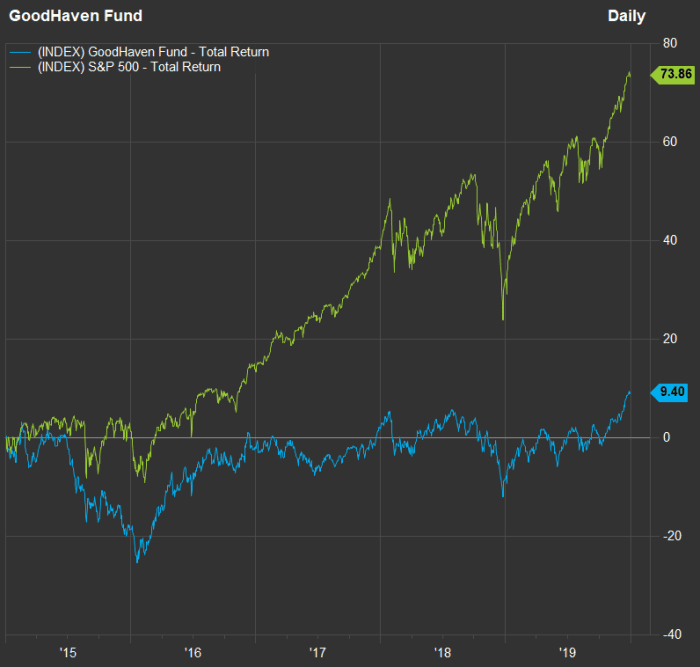

To start, check out how the GoodHaven Fund carried out, with dividends and capital-gains distributions reinvested, over a five-year interval by means of 2019, in contrast with the S&P 500:

For 5 years by means of 2019, the GoodHaven Fund returned solely 9.4%, whereas the S&P 500 returned 73.9%.

FactSet

Late in 2019, Pitkowsky led a collection of adjustments in how the fund operated, together with paying much less consideration to macroeconomic elements, transferring on extra rapidly if investments aren’t figuring out nicely and holding on to profitable corporations longer, to keep away from promoting too early. He cited Microsoft Corp.

MSFT

for instance of a inventory he had parted methods with too early, and stated an instance of an trade and macro-based funding play that didn’t go nicely was a gaggle of power and supplies shares that had been crushed when commodity costs dropped from mid-2014 and 2015 by means of early 2016.

“We like to own high return-on-capital companies” with good trajectories for progress, Pitkowsky stated, “before everyone else has figured it out.”

He added: “We try to avoid structurally challenged businesses that might be statistically cheap.”

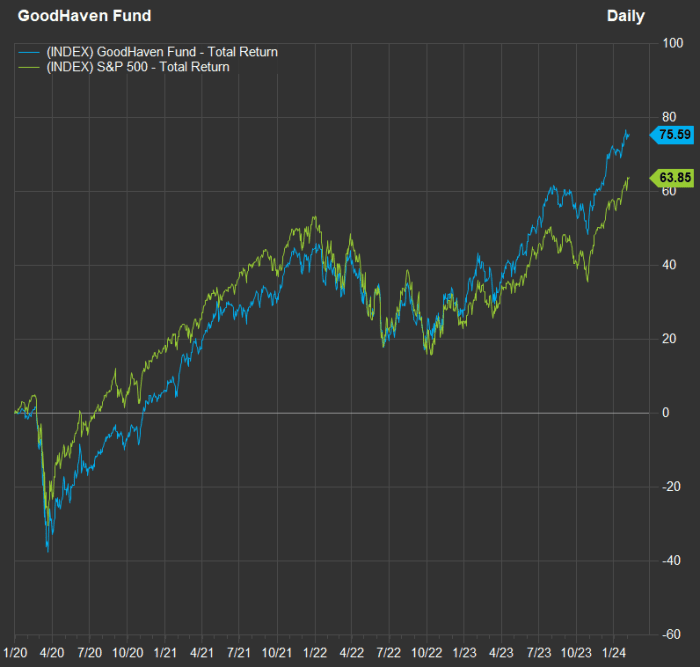

Now check out how the fund has carried out towards the S&P 500

because the finish of 2019:

The GoodHaven Fund has outperformed the S&P 500 since altering its investment-selection course of late in 2019.

FactSet

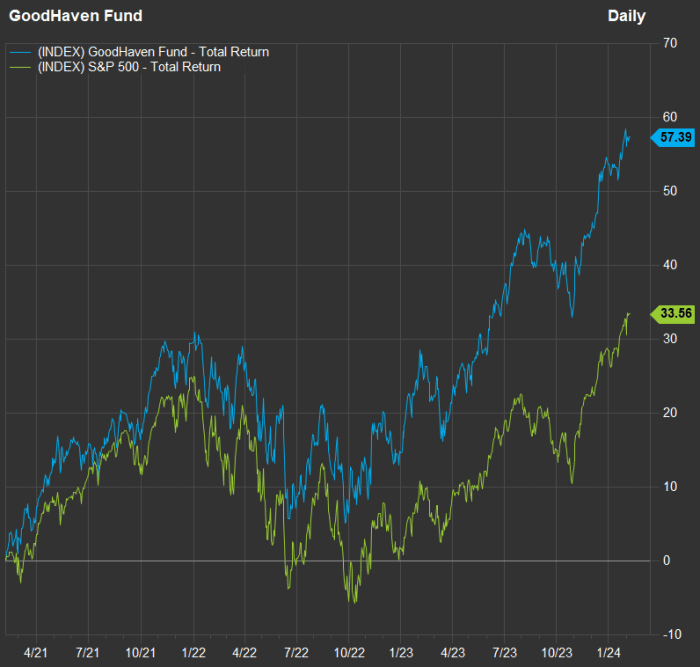

Narrowing additional to a three-year chart by means of Feb. 6 sheds extra mild on the seesaw efficiency of the broad inventory market, with an 18.1% decline for the S&P 500 in 2022 adopted by a 26.3% return in 2023.

The GoodHaven Fund has had a smoother experience in the course of the inventory market’s up-and-down cycle over the previous two years, resulting in a a lot larger three-year return than that of the S&P 500.

FactSet

Fund holdings and feedback about corporations

GoodHaven Capital Management has about $340 million in property underneath administration, together with separate consumer accounts and about $230 million within the fund.

As of Nov. 30, the fund’s portfolio was 29% in money and short-term investments, partly due to an inflow of latest cash from buyers but in addition as a result of Pitkowsky desires to maintain cash available to make purchases at enticing costs and to fulfill any redemption requests from the fund’s shareholders. At instances the fund’s degree of money and short-term investments has been a lot decrease.

Here are the fund’s high 10 stockholdings as of Nov. 30, making up 52% of its portfolio:

| Stock | Ticker | % of fund | Forward P/E |

| Berkshire Hathaway Inc. Class B | BRK | 11.2% | 22.0 |

| Alphabet Inc. Class C | GOOG | 7.0% | 21.1 |

| Builders FirstSource Inc. | BLDR | 6.6% | 14.6 |

| Bank of America Corp. | BAC | 5.4% | 10.3 |

| Devon Energy Corp. | DVN | 4.4% | 7.6 |

| Jefferies Financial Group Inc. | JEF | 4.2% | 11.1 |

| Exor N.V. | NL:EXO | 4.2% | 7.6 |

| Lennar Corp. Class B | LEN | 3.5% | 9.6 |

| Progressive Corp. | PGR | 2.8% | 21.0 |

| KKR & Co. | KKR | 2.8% | 18.5 |

| Sources: GoodHaven Capital Management, FactSet | |||

Click on the tickers for extra about every firm, fund or index.

Click right here for Tomi Kilgore’s detailed information to the wealth of knowledge accessible at no cost on the MarketWatch quote web page.

The desk contains ahead price-to-earnings ratios for the shares, based mostly on Tuesday’s closing value and consensus earnings-per-share estimates for the subsequent 12 months amongst analysts polled by FactSet. For comparability, the S&P 500 trades at a weighted ahead P/E of 20.2.

Two “big wins” Pitkowsky cited when discussing the GoodHaven Fund’s current outperformance had been Builders FirstSource Inc.

BLDR

and the Class B shares of Lennar Corp.

LEN,

a house builder that’s buying and selling at a low P/E, together with its total trade group. We listed P/E ratios for 17 house builders in October, when most of them had been very low. At that point, the S&P Composite 1500 Homebuilding subindustry group was buying and selling at a weighted ahead P/E of seven.6. The group now trades at a ahead P/E of 10.2.

Pitkowsky believes each Builders FirstSource and Lennar have “plenty of growth ahead of them” and stated he was additionally happy that each corporations have low ranges of debt. “The big builders have become much better businesses,” he stated.

Something else to think about is that Pitkowsky holds Lennar’s Class B shares, which commerce at a ahead P/E of 9.6 — a reduction to the valuation of the corporate’s Class A shares

LEN,

which commerce at a ahead P/E of 10.3.

Lennar’s Class B shares have 10 instances the voting rights because the Class A shares, however they commerce at a decrease P/E, in all probability as a result of they’re much less liquid and aren’t included within the S&P 500, Pitkowsky stated. “When we began to research [Lennar], we saw the super-voting shares traded at around a 20% discount to the non-super-voting shares,” he stated, including that the fund has benefited because the valuation hole has narrowed.

Another large winner for the fund has been Bank of America Corp., which Pitkowsky stated was his largest buy in the course of the 12-month interval that ended Nov. 30. Bank of America now trades at a ahead P/E of 10.3, in contrast with a five-year common of 11.1 and a 10-year common of 11.3.

“[Bank of America’s] return on equity is a depressed 11%+,” he wrote within the November letter to GoodHaven Fund shareholders. But he likes the inventory’s danger/reward potential for a number of causes, together with “recurring earnings from the nonbanking businesses.”

While lamenting what he now is aware of was an early sale of Microsoft shares, Pitkowky factors to Alphabet Inc.

GOOGL

GOOG

as a powerful holding he has caught with since 2011.

Alphabet trades on the lowest P/E among the many 10 largest corporations within the S&P 500.

Pitkowsky stated he remained comfy with Alphabet as a big holding, partly as a result of the corporate has change into “more focused over the past year or two on re-engineering the cost base.” He added that the inventory’s valuation “does not seem demanding” relative to Alphabet’s additional progress potential.

Don’t miss: Is Meta now a price inventory?